New Berkeley Lab Report on Solar-Adopter Income and Demographic Trends

Lawrence Berkeley National Laboratory has released the latest edition of its annual report, Residential Solar-Adopter Income and Demographic Trends. The report is based on address-level data for 4.1 million residential households across the country that installed rooftop or other onsite solar through year-end 2023, representing 87% of all U.S. residential PV systems. It describes trends in solar-adopter household income, race and ethnicity, rurality, education levels, occupation, age, home value, housing type and tenure, and prevalence within disadvantaged communities. The report also explores how characteristics of PV installations vary with household income level, including differences in the use of third-party ownership, battery storage, and system size, as well as differences across solar installers in terms of the income profile of their customers.

With its unique size, geographic scope, and level of detail, this report is intended to serve as a foundational reference document for policymakers, industry stakeholders, and researchers. The report is accompanied by an online data visualization tool that enables users to further explore trends at the national, state, county, and census-tract level.

The authors will also host a webinar highlighting key findings from the latest edition of the report on December 18th from 10-11 am Pacific. Register for the webinar here: https://lbnl.zoom.us/webinar/register/WN_LlesicNeQaS3AttKFd4hdg

The following are a few select findings from the latest update:

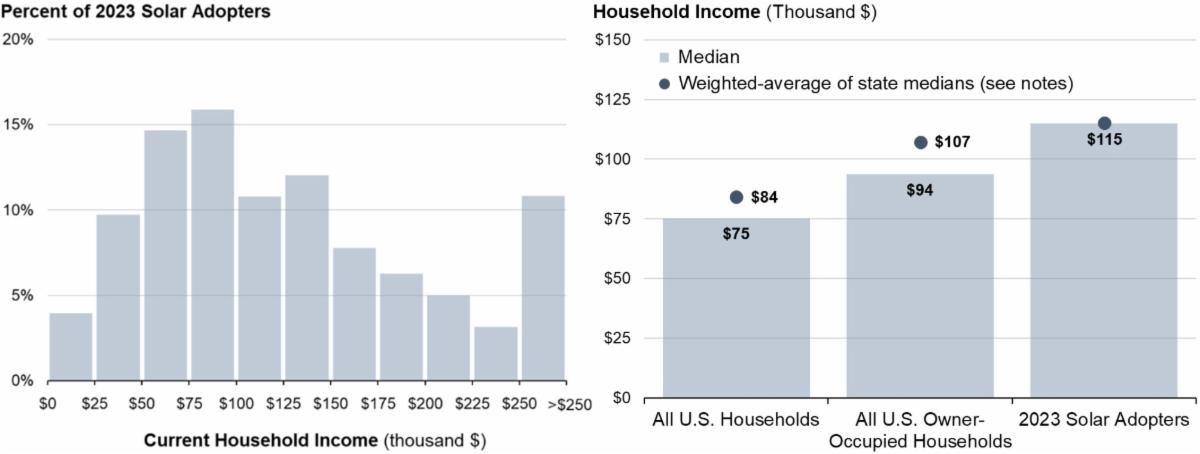

Solar-adopter incomes vary considerably and include many low-and-moderate income households. Solar adopters come from all income groups. As shown in the left-hand panel in Figure 1, 44% of U.S. households that installed solar in 2023 had incomes below $100,000. Though not shown here, 49% of 2023 adopters had incomes below 120% of their area median income (a threshold sometimes used to define low-and-moderate income or LMI).

Figure 1. Solar-adopter income distribution in 2023 (left) and solar-adopter incomes compared to all U.S. households and owner-occupied households (right). Weighted averages in the right-hand figure are the averages of state-level median incomes for each group, weighted by the number of 2023 solar adopters in each state. The purpose of those weighted averages is to provide a basis for comparison that accounts for the concentration of solar adopters within particular states.

Solar-adopter incomes skew high, albeit less so if comparing to only owner-occupied homes in the same state. The median household income of 2023 solar adopters was $115,000, which is 53% higher than the median income of all U.S. households ($75,000), as shown in the right-hand panel of Figure 1. That disparity is due partly to the fact that rooftop solar is largely limited to owner-occupied homes and partly to the concentration of the U.S. solar market in relatively high-income states. Controlling for both of those factors, solar-adopter incomes in 2023 were roughly 7% higher than the median income of owner-occupied households in the same state ($107,000).

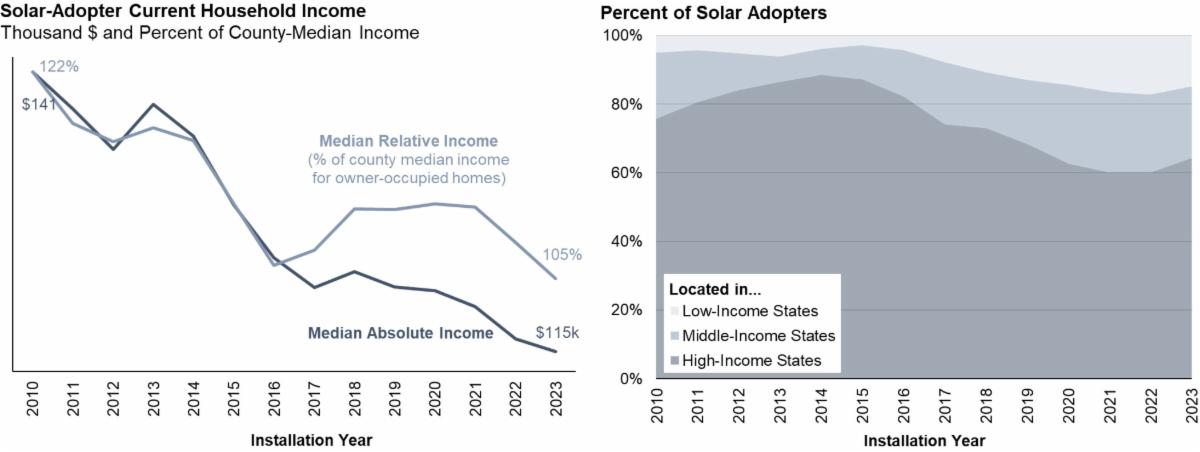

Solar adoption continues to slowly shift toward less affluent households over time. The median income of solar adopters fell from $141,000 in 2010 (based on present-day incomes) to $115,000 in 2023, as shown in the left-hand panel of Figure 2. This overall trend partly reflects a deepening of solar markets, as adoption has increasingly occurred among less affluent households within individual regions. This is reflected in the trajectory of solar-adopter “relative incomes” shown in the left-hand figure, which fell from 122% of their respective county-median incomes in 2010 to 105% in 2023. The declining trend in solar-adopter incomes also reflects a broadening as the U.S. solar market has expanded into low- and middle-income states, as shown in the right-hand panel (albeit with some regression back toward high-income states in 2023).

Figure 2. Temporal trend in solar-adopter median incomes (left) and distribution of solar adopters across states (right). Solar adopter incomes are estimated for the year 2024, regardless of when PV installation occurred and without any inflation adjustment. Relative incomes represent each solar adopter’s income as a percentage of the respective county median income for all owner-occupied households. For the figure on the left, the y-axis has been scaled to focus on just the range over which the values have changed over time. For the figure on the right, states are grouped based on their median household income, with roughly an equal number of households in each group. The distribution in that figure is based on the solar-adopter sample, which slightly over-represents high-income states compared to the total U.S. solar market.

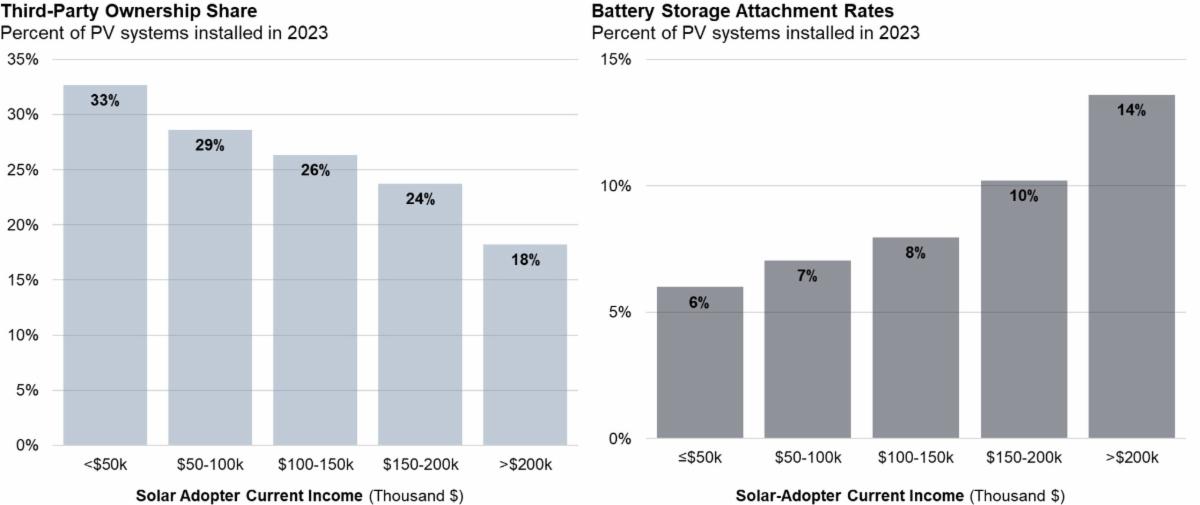

Third-party ownership is more prevalent among lower income solar adopters, compared to higher income adopters. Third-party ownership (TPO) through leases or power purchase agreements is one way to address up-front cost barriers to PV adoption. As shown in the left-hand panel of Figure 3, TPO shares are consistently higher for less affluent households, with almost double the rate for households in the lowest vs. the highest income group in 2023 (33% vs. 18%).

Lower income solar adopters are much less likely than higher income adopters to install battery storage with their PV systems. Customers are increasingly installing battery storage along with their PV systems, which can provide greater utility bill savings and enhanced resilience, albeit with some additional cost. As shown in the right-hand pane of Figure 3, battery storage attachment rates (the percentage of new PV systems co-installed with storage) were consistently lower for less-affluent households in 2023: for the lowest income group, they were less than half the rate of the highest income

Figure 3. Third-party ownership rates (left) and battery storage attachment rates (right) by household income level, for PV systems installed in 2023.

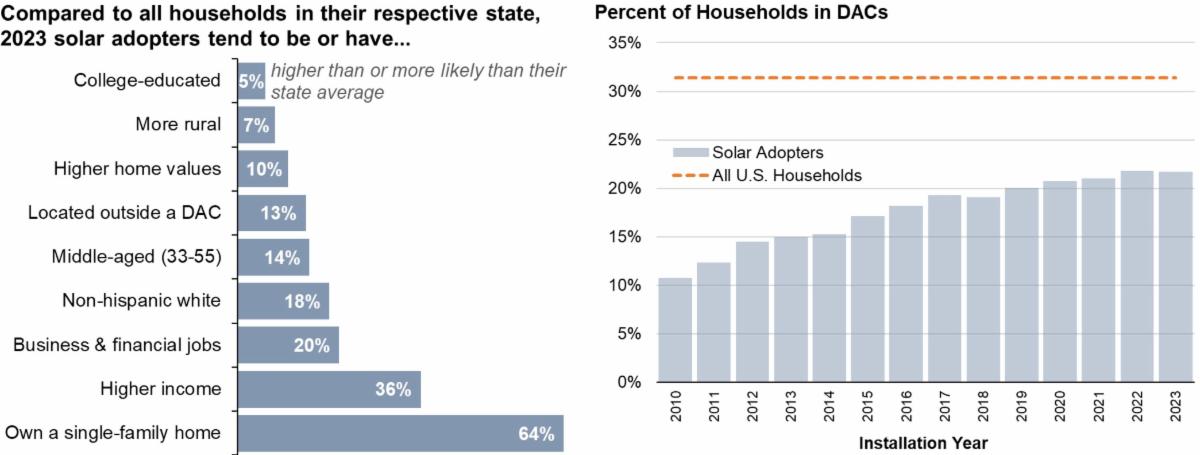

Solar adopters differ from the broader population in terms of other socio-economic attributes beyond income, though those differences are also diminishing over time. As shown in the left-hand panel in Figure 4, compared to all households in their respective state, solar adopters are more likely to: be college educated, live in a rural area, have higher home values, reside outside a disadvantaged community (DAC), be middle-aged, identify as non-Hispanic white, work in a business or financial occupation, and own a single-family home. In all but the last case, the degree of skew is less pronounced than for income. As with income, differences between solar adopters and the broader population are less pronounced (and may even flip directions) when comparing to only owner-occupied households. In addition, most of these differences are shrinking over time, as solar adopters increasingly resemble the broader population. For example, the right-hand panel in Figure 4 shows how the proportion of new solar adopters that reside within DACs has doubled over time, from 11% in 2010 to 22% in 2023, though is still well below the total share of U.S. households within DACs (31%).

Figure 4. Comparison of 2023 solar-adopter socio-economic attributes to all households (left) and percentage of residential solar adopters in disadvantaged communities or DACs (right). For the figure on the left, the percentages were calculated by comparing 2023 solar adopters to all households in their respective state (or county, in the case of home values). Those comparison points were calculated as the average across all U.S. states, weighted by the number of 2023 solar adopters in each state. For the figure on the right, DACs are defined at the census tract level using the U.S. Council on Environmental Quality’s Climate and Economic Justice Screening Tool.

In addition to the various national trends highlighted above, the report also provides state-level trends, and more-granular trends at the county and tract level are available through Berkeley Lab’s online solar demographics tool. Other Berkeley Lab research on topics related to expanding solar access are available at http://solardemographics.lbl.gov.

Lawrence Berkeley National Laboratory | https://emp.lbl.gov/